Start here

If you only read three things, read these.

What HarvestEngine is, why it exists, and why tax-aware direct indexing matters.

3 articles

The math

Tax alpha, fee shape, and the structural differences that change after-tax outcomes.

9 articles

TLH vs ETF rebalancing: which actually saves you money?

Why subscriptions beat percentage-of-assets fees at $250K and up

Tax alpha: the return your portfolio earns by paying less tax

When does the AI Designer + tax-loss math justify the $49?

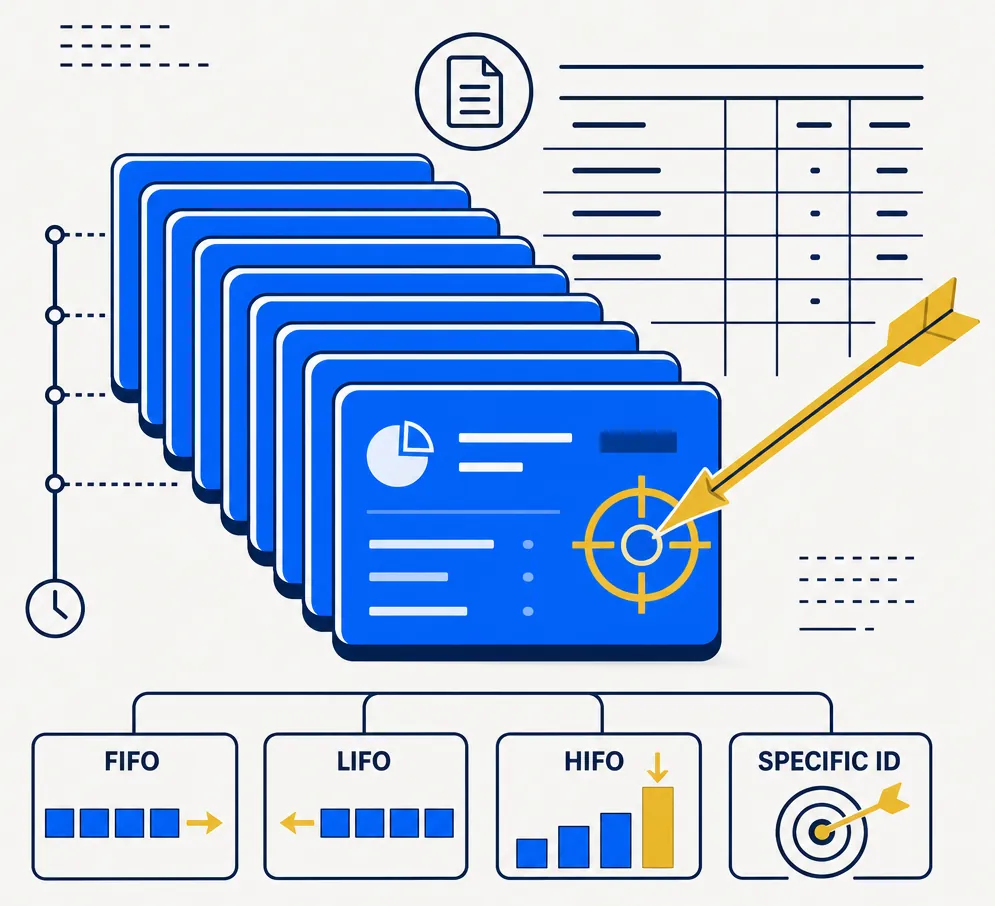

FIFO, LIFO, HIFO, specific-ID: how lot selection changes your tax bill

Capital loss carryforward: how the §1212 carry extends TLH value across years

IRMAA: how Medicare's income surcharge creates a hidden harvest argument

Why ETFs are more tax-efficient than mutual funds in taxable accounts

The 3.8% Net Investment Income Tax: how harvested losses can reduce the surcharge

The rules

Wash sales, basis tracking, and the IRS code sections that decide whether a move is actually clean.

11 articles

The wash-sale rule, demystified

The step-up basis: why long-horizon tax planning is more powerful than it first looks

What counts as 'substantially identical' for §1091?

The IRS code behind tax-loss harvesting: the practical cheat sheet

How TLH interacts with state taxes (California, NY, others)

Dividend washing: when a dividend turns a loss harvest into a problem

Form 8949 walkthrough: how to actually file your harvested losses

Tax-loss harvesting with crypto: the §1091 gap and what to watch

Wash sale rules across spouse accounts: the household pool

Cost basis when you transfer between brokers: the ACAT trap

Alternative Minimum Tax + harvested losses: edge cases

Strategy

Loss banks, pacing, concentrated-stock planning, and advanced overlays in the real world.

10 articles

Concentrated stock + RSUs: tax planning when one ticker dominates

The art of pacing: why timing your harvests through the year matters

The zero-tax exit: pairing losses with gains for a $0 tax bill

Using short positions as escape hatches on risky long bets

When the long sleeve isn't enough

The estate step-up: why holding losers can still be the right call

Donating appreciated stock vs harvesting losses: when each wins

Roth conversions + TLH: timing the year for maximum offset

Should you rebalance in your 401(k) or your taxable account?

Tax-gain harvesting: realizing gains at the 0% rate to reset cost basis

Concepts

The portfolio-construction ideas underneath the product — beta, sleeve structure, direct-index design.

6 articles

Direct indexing in 2026: who needs it, who doesn't

Short overlay: when extra flexibility is worth the complexity

Beta, in plain English: why your portfolio's risk is mostly the market's risk

The three sleeves: beta, long, and short — and why the structure matters

From hand-approve to lights-out — what changes in Autopilot?

Margin, demystified: cash, SMA, and why your buying power is bigger than your cash

The industry

How HarvestEngine compares with the products, platforms, and narratives already in the market.

3 articles