I did not start HarvestEngine because I wanted to become a wealth manager.

I started it because I sat across from one, did the math on the quote in front of me, and could not bring myself to sign.

I have spent my career building and explaining complex systems. That wiring leaks into everything I do. When I look at a product, I want to understand the inputs, the constraints, the tradeoffs, and the expected outputs. I do not like black boxes. I especially do not like black boxes attached to my capital, my taxes, and long-term compounding.

The 1.85% advisor quote was the forcing function that made me pay attention. On a $1M account, that is approximately $18,500 per year. Every year. On a larger account, it gets expensive fast. The service did not get harder as the assets grew. The fee just scaled with the account.

Here is what 1.85% potentially compounds to over time:

| Year | Account value (illustrative, 7% net of fees) | Estimated cumulative fees |

|---|---|---|

| 1 | ~$1,070,000 | ~$18,500 |

| 5 | ~$1,403,000 | ~$117,000 |

| 10 | ~$1,967,000 | ~$295,000 |

| 20 | ~$3,870,000 | ~$847,000 |

| 30 | ~$7,612,000 | ~$1,937,000 |

That math got my attention. But the fee was only the surface of the problem.

What I found when I looked under the hood

What was the real problem with wealth management software beyond the high fee percentage?

Once I started digging, I realized the real issue was not just price. It was architecture — the structure of the product, who held custody, and whether the investor could actually see the logic.

I read everything I could find about tax-loss harvesting, direct indexing, and what the industry called tax alpha. The idea itself made immediate sense to me: instead of treating taxes like an after-the-fact accounting problem, you design the portfolio so taxes are part of the operating system from day one.

Then I looked at the actual market.

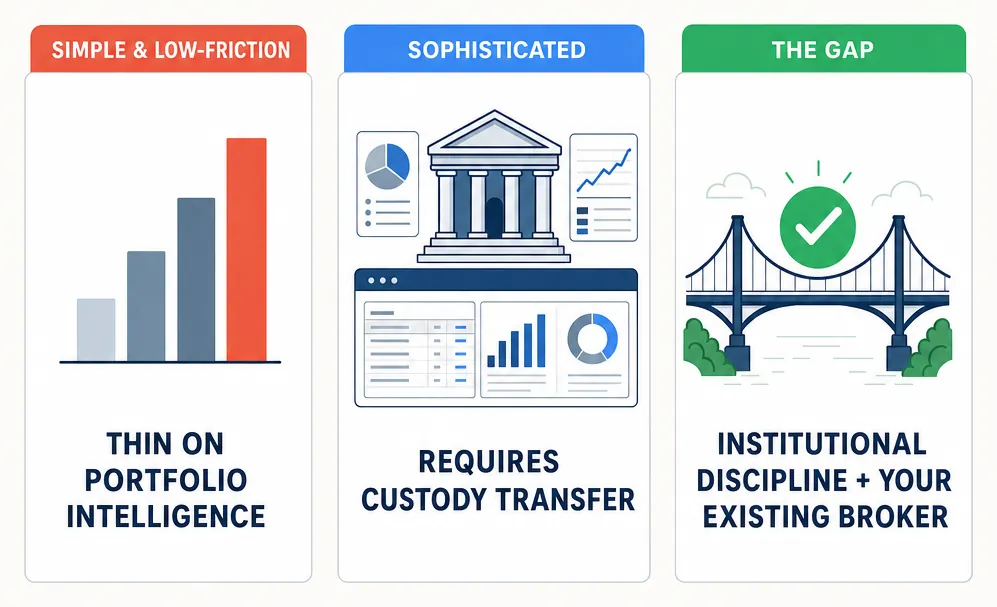

- Some solutions were simple and low-friction, but thin on portfolio intelligence.

- Some had real sophistication, but required custody transfer and a percentage-of-assets fee forever.

- Some private or advisor-led structures clearly had more advanced machinery, but the economics, disclosures, and control model were not built for a self-directed investor who wants to see the logic.

The more I looked, the clearer it became: there was no product that combined institutional discipline with software transparency on the brokerage I already used.

The product I wanted

What kind of tax-aware portfolio software was missing from the market for self-directed investors?

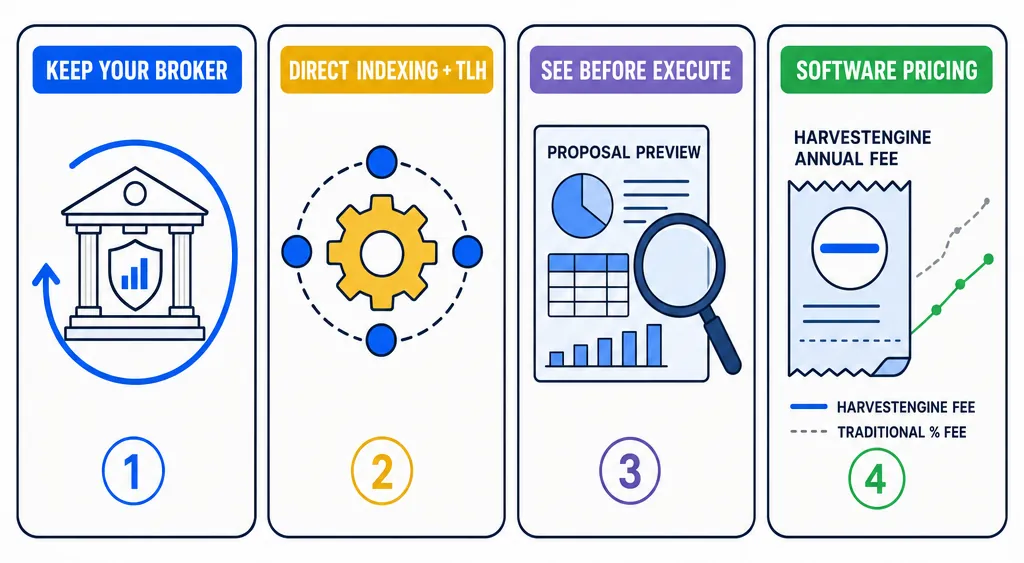

What I actually wanted was straightforward: keep existing brokerage accounts, run direct indexing and tax-loss harvesting on top of them, see the trade rationale before anything executes, and pay software pricing — not a percentage of the portfolio every year.

- Keep my money at the brokerage I already use.

- Run direct indexing and tax-loss harvesting on top of it.

- See why a trade is being proposed before it happens.

- Pay software pricing, not a percentage of my portfolio every year.

I wanted a system that thinks at the portfolio level, not just the position level. A system that understands tax lots, wash-sale risk, replacement quality, and tracking error. A system that gives the investor a reviewable proposal instead of a black-box promise.

It did not exist. So I built it.

Why HarvestEngine exists

Who is HarvestEngine built for, and what distinguishes it from traditional wealth management?

HarvestEngine is for serious self-directed investors who want institutional-style discipline without giving up custody, visibility, or control.

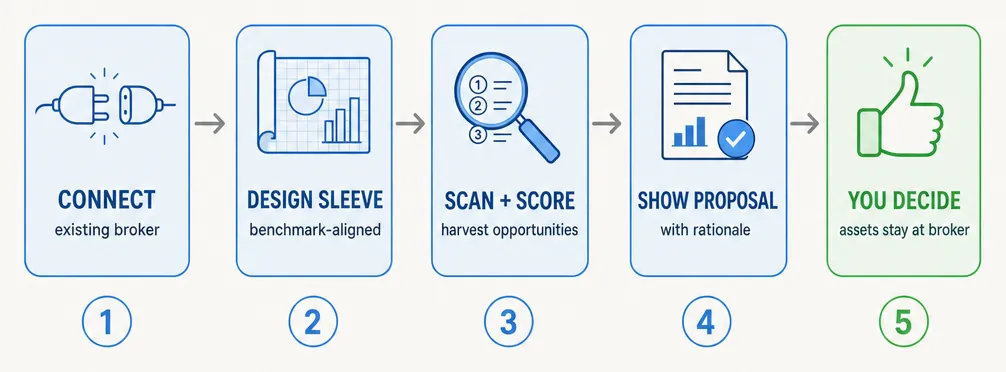

You connect your existing brokerage. We help design a direct-index sleeve aligned to your target benchmark. We look for harvest opportunities, score replacements, track wash-sale windows, and show you the tradeoffs clearly. You stay in control. Your assets stay where they are.

The subscription model matters too. I did not want the economics of the product to get worse as the customer succeeded. The more I thought about it, the more obvious it became that subscription pricing beats percentage-of-assets pricing for the exact kind of investor this product is built for.

What changed my conviction

What ultimately convinced me this product needed to exist and that a software-first approach was right?

The final push came when I realized the gap was not theoretical. The industry already proved there was value in tax-aware overlays and direct indexing. What it had not built was the clean self-directed version — the one where the investor can read the algorithm, audit the trades, and own the decision.

That became the company thesis:

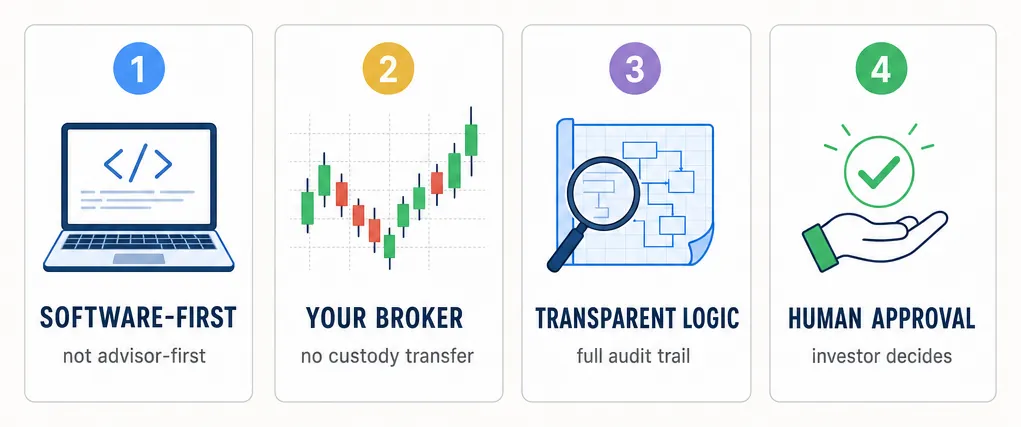

- software-first, not advisor-first

- connected to your broker, not custody transfer by default

- transparent logic, not hidden manager process

- human approval and clear boundaries, not vague automation

That is also why we are explicit about what we are and what we are not. HarvestEngine is software, not a registered investment advisor. We do not take custody of your money. We do not sell you a discretionary relationship wrapped in softer language. We help you run a better tax-aware process on the accounts you already own.

The founder story, honestly

What is the real reason HarvestEngine exists beyond the initial advisor fee quote?

So yes, the 1.85% number is part of the story. It was the hook. It made the problem impossible to ignore.

But the deeper founder story is this: I wanted a product that treated tax-aware portfolio management the way a good engineer treats any serious system problem. Clean inputs. Clear assumptions. Measurable outputs. No fairy dust. Read the actual algorithm if you want to see the difference.

That product did not exist in the form I wanted.

Now it does.

—KyleA

Founder, HarvestEngine