Most investors focus on returns and ignore fee shape. That is a mistake.

A flat subscription and an assets-under-management fee — usually shortened to AUM fee, a yearly charge calculated as a percentage of your whole portfolio — can both look reasonable in year one. Over time, they behave very differently. One stays fixed. The other scales with your wealth forever.

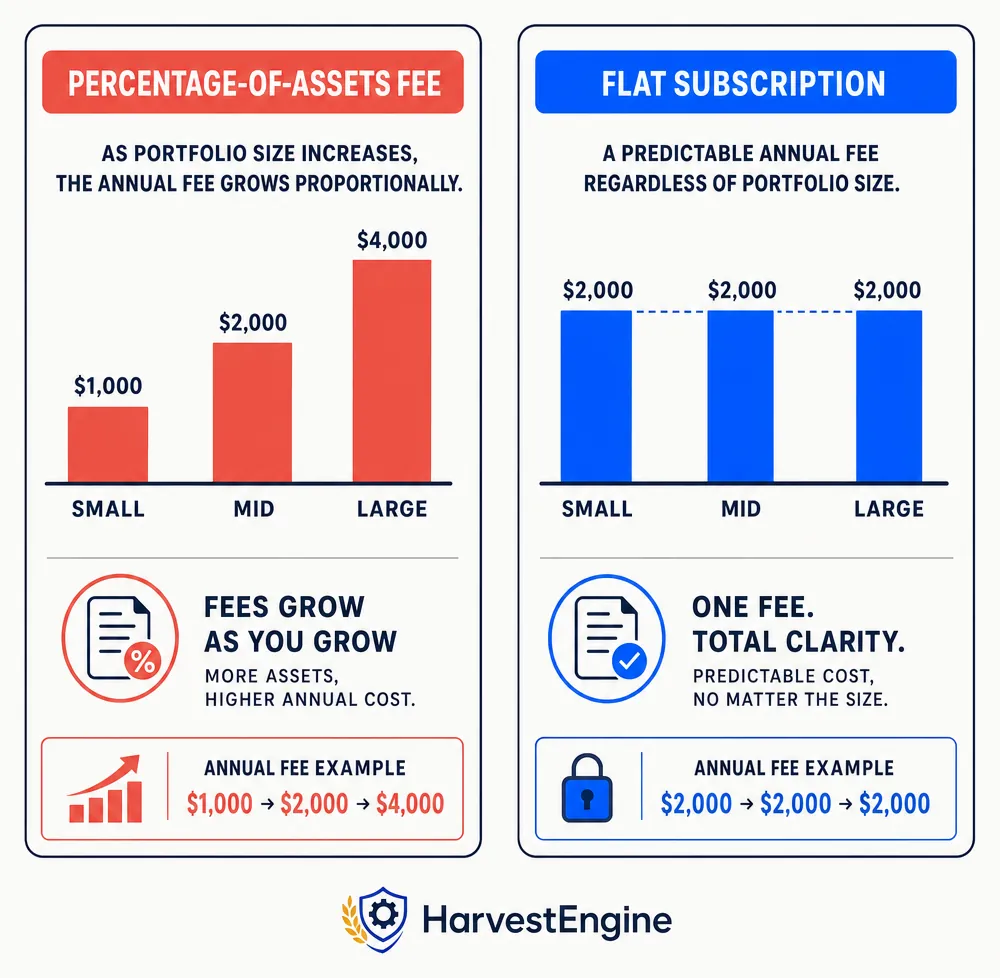

The two models

- AUM fee (assets-under-management fee): a percentage of the account every year

- Subscription: a fixed dollar fee every month

Why does an AUM fee behave so differently from a flat subscription over time?

The percentage model feels small — that is exactly why it is powerful for the firm. As the account compounds, the fee compounds with it, silently scaling without the product getting harder to deliver.

The subscription model does the opposite. If the account grows, the software does not automatically get a larger cut.

The crossover is the decision point

At what account size does a flat subscription typically become cheaper than a percentage-of-assets fee?

The most important number is the crossover — the account size where the annual AUM fee becomes more expensive than the annual subscription. The table below uses HarvestEngine's annual rate (approximately $49/mo = $490/yr, $99/mo = $990/yr, $199/mo = $1,990/yr with 2 months free).

| AUM rate | Crossover at Guided ($490/yr) | Crossover at Autopilot ($990/yr) | Crossover at Alpha ($1,990/yr) |

|---|---|---|---|

| 0.25% | $196K | $396K | $796K |

| 0.40% | $122.5K | $247.5K | $497.5K |

| 1.00% | $49K | $99K | $199K |

| 1.85% | $26.5K | $53.5K | $107.6K |

That last row is the wake-up call. Once you are paying legacy advisor economics, even a relatively expensive software tier beats the AUM model at surprisingly small account sizes.

See it yourself

The part people underweight

What is the hidden cost of percentage-based fees beyond the annual dollar charge itself?

The visible fee is one thing. The lost compounding on that fee — the capital removed from the account that would otherwise keep growing — is potentially the bigger long-term cost.

When the platform takes a percentage of your assets every year, it is not just collecting dollars. It is also removing dollars that would otherwise keep compounding for you.

That is why a small percentage can turn into a very large wealth transfer over time.

Why people still choose AUM anyway

- It feels invisible. A quarterly deduction is less emotionally obvious than a monthly subscription.

- It is often bundled. People may be paying for a relationship, planning, custody, and convenience, not just one software function.

- It is familiar. The industry normalized percentages, so they sound more respectable than they should.

Why HarvestEngine uses subscription pricing

Why does HarvestEngine use subscription pricing instead of a percentage of assets under management?

HarvestEngine is built on a simple belief: tax-aware portfolio software should be priced like software — flat tiers, the same workflow regardless of account size, and no built-in penalty for wealth growth.

- feature-based tiers

- same workflow regardless of account size

- no built-in penalty for growing your wealth

That is not just cheaper at scale. It is cleaner incentive design.

Read this next with the founder story, HarvestEngine vs Wealthfront, why big firms push TLH, and the per-portfolio threshold math: when does the AI Designer + tax math justify the $49?