Roth conversions and tax-loss harvesting address different parts of the tax picture. A Roth conversion adds ordinary income in the year of conversion. Capital loss harvesting reduces capital gain income. These two strategies do not directly cancel each other out — but when coordinated deliberately, they can leave an investor in a materially better position than either strategy pursued in isolation.

The interaction is subtle enough that it is worth working through carefully. Harvested losses do not simply "offset" conversion income the way intuition might suggest. But they can create bracket space that makes a conversion more efficient — and they interact directly with the Net Investment Income Tax in ways that compound the potential savings.

What makes a Roth conversion a tax-planning challenge?

What makes a Roth conversion a tax-planning challenge for investors?

A Roth conversion adds the full converted amount to ordinary income in the conversion year, which can push income into a higher marginal bracket, trigger the Net Investment Income Tax surcharge, or increase exposure to other income-based phaseouts — making the size and timing of conversions one of the most consequential tax decisions in any given year.

Traditional IRA and pre-tax 401(k) assets grow tax-deferred but are fully taxable as ordinary income when distributed. Converting those assets to a Roth account means paying those taxes now — at today's rates — in exchange for future tax-free growth and the elimination of required minimum distributions. The long-run appeal can be significant. So is the tax bill in the conversion year.

The planning challenge is that ordinary income from a conversion is additive. It stacks on top of wages, Social Security, rental income, and capital gains. In a year with significant capital gains — from rebalancing, a large sale, or equity compensation — an uncoordinated conversion may push combined income into a bracket the investor did not intend to reach.

How do capital losses interact with Roth conversion income?

Can harvested capital losses directly offset the ordinary income recognized from a Roth conversion?

Capital losses generally cannot directly offset ordinary income from a Roth conversion — under IRC §1211, capital losses must first offset capital gains, and only up to $3,000 of any remaining net capital loss may reduce ordinary income in a given tax year, with excess carried forward to future years.

This is an important boundary to understand clearly. If an investor harvests capital losses in a year when they also do a Roth conversion, the two do not directly cancel each other out. The harvested losses reduce capital gain income. The Roth conversion income remains ordinary income and is taxed as such.

The annual deduction of up to $3,000 against ordinary income is a modest direct benefit. For investors in higher brackets, it may represent a saving of approximately $700–$1,300 depending on marginal rate — useful, but not the primary mechanism by which TLH interacts with Roth conversions.

How does TLH create room for a larger Roth conversion?

How does tax-loss harvesting potentially create room for a larger Roth conversion within the same marginal bracket?

By using harvested losses to cancel out capital gains that would otherwise occupy marginal bracket space, TLH can lower total taxable income and may leave room to convert more traditional IRA assets at a lower effective rate — the same bracket is being used for a more efficient purpose when gain income is cleared first.

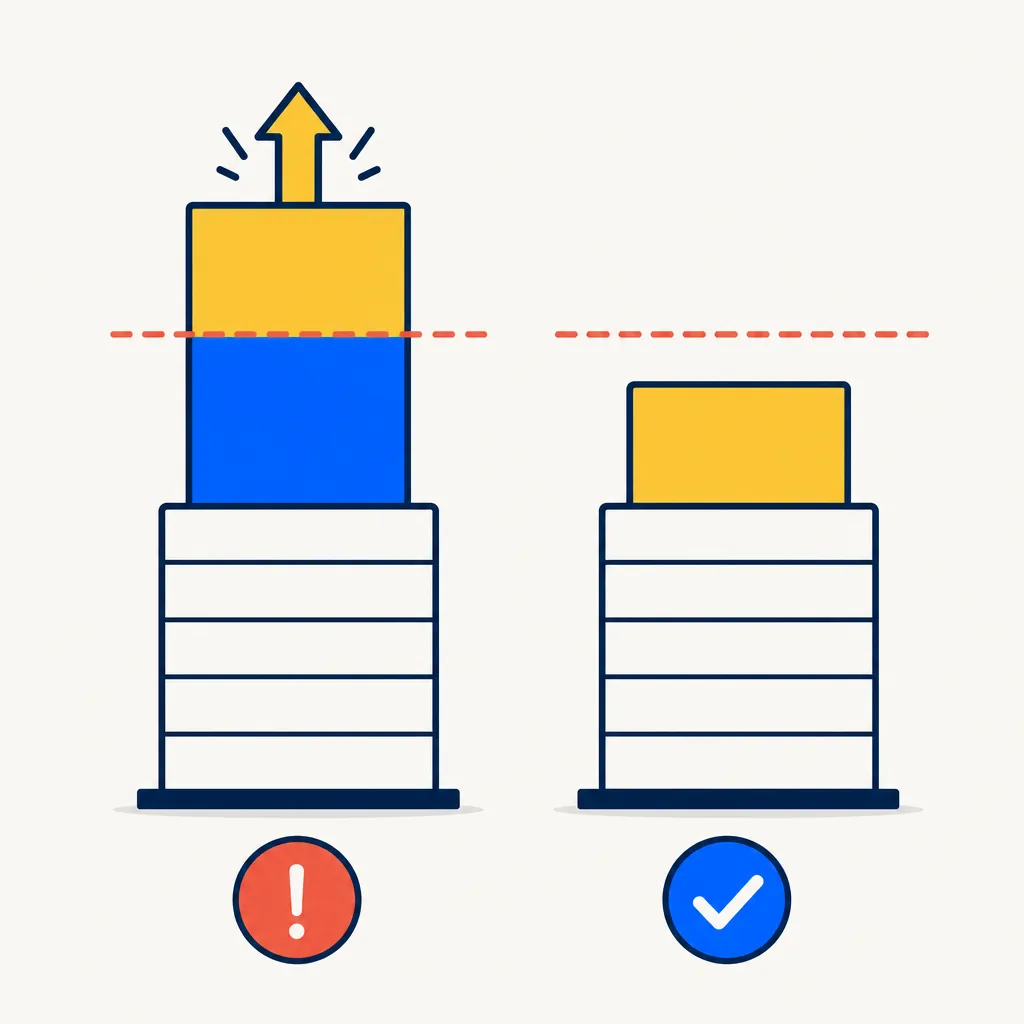

Consider a simplified illustration. An investor expects approximately $40,000 in realized capital gains from a rebalancing event. Without TLH, those gains occupy the top of the investor's current bracket. Adding a Roth conversion on top of those gains pushes conversion income into the next bracket.

If the investor also harvests approximately $40,000 in capital losses, net capital gain falls to approximately zero. The bracket headroom that was occupied by those gains is now available for the Roth conversion. The conversion amount fills that space at the lower rate rather than the higher one. The same dollars of conversion income are taxed at a potentially lower marginal rate simply because the composition of taxable income changed.

This dynamic can be most valuable in years when the investor has both harvestable losses available and planned conversion activity. The annual TLH pacing article covers how to inventory available losses and plan the year's harvest activity — the same planning rhythm applies when a Roth conversion is also on the agenda.

How does NIIT interact with TLH in a Roth conversion year?

How does tax-loss harvesting interact with the Net Investment Income Tax in a year when a Roth conversion also occurs?

The Net Investment Income Tax under IRC §1411 applies a surcharge on net investment income above a modified AGI threshold; harvested capital losses reduce net investment income directly and can reduce or eliminate this surcharge on gains recognized in the same year, even in a year when a Roth conversion also occurs.

NIIT is a separate layer on top of capital gains taxes. It applies specifically to net investment income — meaning capital losses that offset capital gains reduce the NIIT base directly. The surcharge applies above modified AGI thresholds of approximately $200,000 for single filers and approximately $250,000 for married filing jointly under current IRC §1411 rules.

In a Roth conversion year, the interaction becomes more nuanced: the conversion income itself is ordinary income, not investment income, so it does not directly enter the NIIT calculation. But the conversion can push modified AGI above the NIIT threshold, making capital gains in that year more likely to attract the surcharge.

Harvested capital losses that reduce capital gain income can therefore serve a dual function in a Roth conversion year: they reduce the net capital gain potentially subject to NIIT, and they free up bracket space for the conversion. The tax code references most relevant here are IRC §1411 (NIIT), IRC §1211 (capital loss limitations), and the Roth conversion rules under IRC §408A. The IRS code cheat sheet covers these sections in accessible terms.

When in the year should investors coordinate these two strategies?

What is the ideal timing within the calendar year for coordinating a Roth conversion with a tax-loss harvesting plan?

Because total income for the year is not known until year-end, many practitioners consider a late-year approach to sizing the final conversion amount — after inventorying realized gains, harvested losses, other income sources, and current bracket position — while recognizing that harvest opportunities are market-driven and occur throughout the year.

In practice, the two strategies operate on different timelines. Harvest opportunities appear when positions move into loss territory — which is market-driven and difficult to predict. Roth conversions can be timed more deliberately because the investor controls when and how much to convert.

A common approach is to harvest losses throughout the year as they become available, then assess the Roth conversion opportunity in the fourth quarter once the year's realized income picture is clearer. At that point, an investor can model the combined income picture: wages plus other income, plus net capital gains after harvests, plus any planned conversion amount. The conversion can then be sized to stay within a target bracket rather than exceed it inadvertently.

Partial conversions — converting a portion of a traditional IRA rather than the full balance — are permitted under IRC §408A and can be useful for staying within a specific bracket threshold. The tax alpha article discusses how the compounding value of bracket management across many years may add meaningful after-tax improvement over time.

What mistakes are common when combining these strategies?

What are the most common mistakes investors make when combining Roth conversions and tax-loss harvesting in the same tax year?

The most common mistakes are treating the two strategies independently rather than jointly, converting without first accounting for capital gains that will also appear on the return, and over-converting in a year with minimal harvestable losses — where the conversion crosses into a higher bracket with no gain-clearing offset available.

A few specific patterns worth noting:

- Treating losses as a direct offset to conversion income. As described above, capital losses cannot directly zero out Roth conversion income beyond the limited annual deduction. Investors who assume otherwise may convert more than intended at a higher marginal rate.

- Ignoring state tax interaction. Roth conversions are also taxable at the state level in most conforming states. In high-tax states, a larger conversion may face a combined marginal rate well above the federal rate alone. The state taxes article covers how TLH interacts with state-level capital gains treatment.

- Under-harvesting in a conversion year. In a year when a significant conversion is planned, having additional harvested losses to offset capital gains can be particularly valuable. Investors who only harvest reactively may leave bracket-clearing opportunities on the table.

- Converting in a year with unusually high capital gains. The same year an investor takes a large concentrated-stock gain, receives significant equity compensation income, or realizes large gains from rebalancing is often a challenging time for a large Roth conversion — unless paired with a substantial harvest offset. The zero-tax exit strategy article covers how a loss bank can be paired with intentional gain realization across multiple years.

Read this next with annual TLH pacing, tax alpha explained, the zero-tax exit strategy, the IRS code cheat sheet, TLH and state taxes, rebalancing in a 401(k) vs taxable account, and the NIIT and TLH.