Rebalancing is one of the most common portfolio maintenance tasks — selling positions that have drifted above target weight and buying those that have drifted below. Inside a 401(k) or IRA, the transaction has no immediate tax consequence. In a taxable brokerage account, the same trade may produce a capital gains bill at the moment of sale. The decision about which account absorbs each rebalancing trade is one of the most tax-efficient choices an investor makes on a recurring basis.

For investors running a direct-index sleeve alongside a tax-advantaged account, the question has an additional dimension: the taxable account may be the right venue to rebalance not because it avoids taxes, but because tax-loss harvesting can accomplish the rebalancing at zero marginal tax cost when done correctly.

Why does rebalancing in a taxable account trigger a tax event?

Why does rebalancing in a taxable brokerage account create a taxable event while the same trade inside a 401(k) does not?

When appreciated securities are sold in a taxable brokerage account, the gain is recognized immediately as a capital gain under IRC §1001 and reported on Schedule D — whereas trades inside a 401(k), traditional IRA, or Roth IRA occur within a tax-sheltered wrapper where gains are not recognized until distribution, or not at all in the case of a Roth.

The mechanics of capital gains recognition make every sell in a taxable account a potential tax event. If a position was purchased at a certain price and has risen since, that gain is recognized the moment the sale settles. Positions held more than one year qualify for long-term capital gains rates under IRC §1(h); positions held one year or less are taxed at ordinary income rates. Neither threshold applies inside a tax-sheltered account.

The structural difference flows from the account type. A 401(k) is governed by IRC §401(a); a traditional IRA by IRC §408. Growth, dividends, and realized gains inside these accounts accumulate without annual tax consequence. The investor pays taxes when distributions are taken — or pays nothing on qualified Roth distributions under IRC §408A. The tax obligation is deferred; how beneficial that deferral is depends on the investor's current and future marginal rates.

How does rebalancing inside a 401(k) or IRA avoid that cost?

What makes tax-advantaged accounts a natural venue for rebalancing when minimizing tax friction is the goal?

Because gains and losses inside a 401(k) or IRA do not generate a current-year tax event, investors can sell overweight positions and buy underweight ones freely, without concern for holding period, cost basis, or marginal rate — the tax cost is deferred or eliminated entirely depending on the account type.

This makes tax-advantaged accounts the preferred rebalancing venue for routine portfolio maintenance. If an equity allocation has drifted up relative to bonds, selling equities inside a 401(k) and buying bonds there costs nothing in current-year taxes. The same trade in a taxable account would recognize potentially years of accumulated gain at the moment of sale.

A practical implication: when an investor holds both a 401(k) and a taxable account, routing rebalancing trades to the tax-advantaged side tends to produce a lower cumulative tax burden over many years. Many portfolio management frameworks start from this principle — rebalance where the tax cost is zero, and only involve the taxable account when necessary or strategically advantageous.

The lot selection article discusses how cost-basis accounting methods affect which lots are sold when a taxable-account sale does become necessary — an important secondary consideration once a rebalancing trade must cross into the taxable side.

What is asset location, and how does it shape the rebalancing decision?

What is the asset location principle, and how does it affect where different asset classes should be held and consequently where rebalancing trades should occur?

Asset location refers to the decision about which account type holds each asset class: tax-inefficient assets — those that generate high ordinary income or short-term gains — may be better placed inside tax-advantaged accounts, while tax-efficient equity positions may fit more naturally in taxable accounts, and this arrangement shapes which account can absorb rebalancing with the least tax friction.

The classic asset location framework places high-income or high-turnover assets — such as bonds paying ordinary interest, REITs, and actively traded funds — inside the 401(k) or IRA where the income is sheltered from annual taxation. Tax-efficient assets — those with low turnover, qualified dividends, and long-term gain profiles — go in the taxable account where their low taxable activity is well-matched to the account type. This arrangement may reduce annual tax drag on the overall portfolio.

The rebalancing decision follows from location. If bonds are held in the 401(k) and equities in the taxable account, correcting a drift toward equities is often handled primarily by increasing the bond allocation inside the 401(k) — rather than by selling equities in the taxable account. When the drift is entirely within the tax-advantaged account, correction stays inside the shelter with no immediate tax consequence.

Location decisions also interact with rebalancing frequency. Accounts with high natural activity — due to regular contributions, distributions, or higher-turnover strategies — can generate more taxable events over time when they sit in the taxable account. The annual pacing article covers how deliberate timing of harvest activity can create a structured approach to taxable-account activity throughout the year.

When does the taxable account become the right rebalancing venue?

Under what circumstances does it make sense to rebalance within the taxable account despite the potential capital gains cost?

The taxable account may become the better rebalancing venue when tax-loss harvesting opportunities are available — specifically when the rebalancing sell is itself a loss, or can be paired with a harvesting trade that resets basis while maintaining market exposure, potentially achieving the rebalancing at a reduced or zero net tax cost.

The clearest case is when the target correction can be accomplished by selling a position trading at a loss. The sale harvests the loss, reduces exposure to the overweight position, and if the proceeds are deployed into a replacement holding with similar (but not substantially identical) exposure under IRC §1091's wash-sale framework, the portfolio moves back toward its target weights without triggering a gain. The harvested loss may then offset capital gains recognized elsewhere in the portfolio or in prior and future years under IRC §1212.

A different case arises when an investor receives regular contributions into the taxable account — from wages, equity compensation vesting, or other inflows. Directing contributions toward underweight positions is a form of rebalancing that requires no sell at all. This approach can keep the taxable account close to target weights over time without generating any capital gains.

The Roth conversion and TLH article covers a related coordination scenario: when taxable-account rebalancing interacts with other income events in the same tax year, such as conversion income that affects marginal bracket position.

How does tax-loss harvesting change the rebalancing calculus in the taxable account?

How does tax-loss harvesting potentially transform taxable-account rebalancing from a tax-generating event into a tax-reducing one?

Tax-loss harvesting may convert the tax cost of rebalancing into a tax benefit when positions designated for the rebalancing sell are trading below their cost basis — the sale generates a harvestable capital loss that may then offset capital gains elsewhere in the portfolio, potentially making the rebalancing trade net-positive from a tax perspective rather than net-negative.

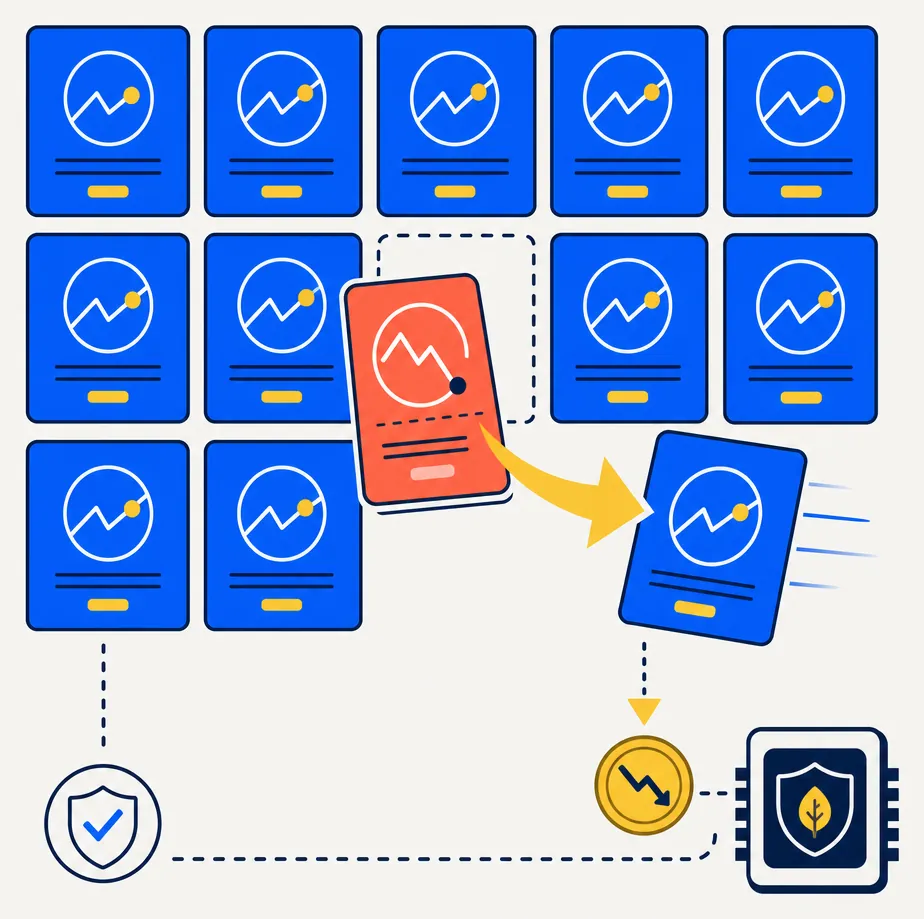

This is where the direct-index structure of a taxable sleeve becomes particularly useful. A portfolio of individual securities typically has positions trading at losses even during broad market rises — individual names diverge, sectors rotate, and cost-basis lots from different purchase dates create variation within the same holding. A broad index ETF, by contrast, offers only one harvest surface: the ETF itself. If the ETF has appreciated since purchase, every rebalancing sell from that position is a taxable gain.

HarvestEngine's lot selection logic identifies which specific lots minimize tax cost when a rebalancing sell is required — preferring loss lots, then high-cost-basis lots, then deferring to the user's specified accounting method for the remainder. Evaluating at the lot level, rather than the position level, can substantially reduce the effective tax cost of an otherwise gain-generating rebalance.

The interaction with long-horizon planning is also relevant. A well-maintained loss bank from ongoing harvesting activity can offset gains from rebalancing in future years, not just the current one. A harvested loss realized today carries forward under IRC §1212 and can be applied against a gain-generating rebalancing trade in a year when the portfolio has appreciated more broadly. The zero-tax exit strategy article covers how loss carry-forwards can be paired with intentional gain realization across multiple years.

What are the practical trade-offs between the two rebalancing venues?

What are the main practical trade-offs between routing rebalancing to the tax-advantaged account versus the taxable account?

Rebalancing in the tax-advantaged account avoids current-year capital gains but cannot generate harvested losses that offset gains elsewhere; rebalancing in the taxable account may trigger current-year gains but also creates harvest opportunities — the optimal routing depends on whether specific positions are at a gain or a loss, the available tax-loss inventory, and the holding-period status of the lots involved.

A simplified decision framework:

| Scenario | Preferred venue | Primary reason |

|---|---|---|

| Correction achievable entirely within the 401(k) or IRA | 401(k)/IRA | Zero current-year tax cost |

| Overweight position trading at a loss in the taxable sleeve | Taxable | Harvest opportunity; loss may offset other gains |

| Correction via new contributions to the taxable account | Taxable (no sell required) | Underweight positions receive inflows; no capital gains event |

| Drift must be corrected across both accounts; some taxable gain unavoidable | Tax-advantaged first, then taxable | Route as much correction as possible through the shelter before the taxable account |

The decision is rarely all-or-nothing. Many investors maintain both a 401(k) and a taxable account, and rebalancing can often be split: absorb as much drift correction as possible inside the tax-advantaged account; handle only the portion that cannot be corrected there in the taxable account, using harvesting opportunities when available.

The tax alpha article covers how these routing decisions compound over many years: the after-tax difference between systematically preferring low-tax rebalancing venues and defaulting to the taxable account may be meaningful in cumulative terms, even when each individual rebalancing event appears modest.

Read this next with tax alpha explained, annual TLH pacing, Roth conversions + TLH, TLH vs ETF rebalancing, and the zero-tax exit strategy.