The wash-sale rule's most overlooked dimension is its reach across the household. Most investors think of IRC §1091 as a one-account timing problem: sell at a loss, wait 31 days, buy back. That framing misses the household-pool logic — two accounts at two different brokerages, held by two different Social Security numbers, can still interact under §1091 in ways that disallow losses in one account based on purchases made in the other.

Revenue Ruling 2008-5 is the governing authority. It extends the wash-sale framework from a single-account analysis to a household-level one — and it has consequences for the majority of two-income households doing tax-aware investing across joint, individual, and retirement accounts.

What did Revenue Ruling 2008-5 establish about spousal accounts?

What did Revenue Ruling 2008-5 establish about how the wash-sale rule applies to a spouse's brokerage account or IRA?

Revenue Ruling 2008-5 holds that a purchase of a substantially identical security in a spouse's account — or in an IRA held by either spouse — within the 61-day wash-sale window disallows the taxpayer's capital loss, regardless of whether the accounts are at separate brokerages or held in different names.

The IRS's reasoning drew on §267's related-party loss-disallowance framework, which treats spouses as a unified household for certain tax purposes. The ruling extended that logic to §1091's wash-sale window: if a spouse buys a substantially identical security within 30 days before or after the loss sale, the loss may be disallowed — just as if the taxpayer had made the purchase themselves.

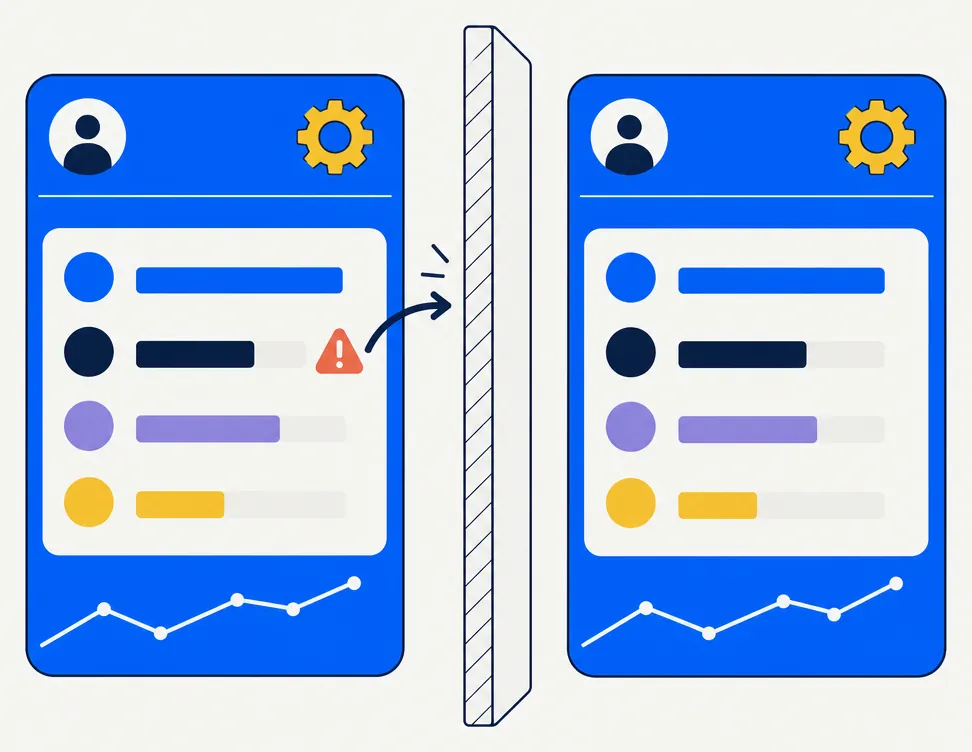

The ruling is important not because it creates a new tax but because it extends a pre-existing rule into territory many investors have not mapped. A household that manages accounts independently, without any shared visibility into trades, is exposed to wash-sale outcomes that neither account's brokerage can detect on its own. For the foundational mechanics of the wash-sale rule — the 61-day window, what "disallowed" means, and the substantially-identical standard — the wash-sale rule, demystified is the right starting point.

Which accounts fall inside the household wash-sale pool?

Beyond a spouse's taxable brokerage account, which account types fall inside the household wash-sale pool under current IRS guidance?

The household pool includes a spouse's individual taxable accounts, traditional and Roth IRAs held by either spouse, and jointly-owned taxable accounts — with IRA purchases carrying a potentially worse outcome than taxable-account wash sales because the basis carryover mechanism that normally defers the disallowed loss may not apply.

Account types most commonly in scope:

- Spouse's individual taxable brokerage account. The direct case in Rev. Rul. 2008-5: a buy here may trigger the wash-sale rule against a loss sale in the other spouse's taxable account.

- IRAs — traditional and Roth. The ruling addresses same-taxpayer IRA purchases directly. Practitioners widely extend the household logic to spousal IRAs by analogy with §267's related-party framework.

- Joint taxable accounts. Both spouses are economic owners of every position in a jointly-owned account — same-symbol purchases here are clearly inside the household pool.

- Custodial accounts for minor children. Generally treated as separate under §267's definitions; children are not spouses. Many practitioners apply a conservative read and include accounts where a parent exercises effective trading control.

The edges here are not all settled by direct authority. For a broader map of the code sections underpinning these rules, the IRS code TLH cheat sheet covers the key provisions in plain English.

The IRA trap: when a spouse's retirement account may destroy a loss

What happens when a purchase in a spouse's IRA triggers the wash-sale rule on a taxable-account loss — and why is it potentially worse than an ordinary taxable-account wash sale?

When the replacement purchase triggering the wash sale is inside an IRA, the disallowed loss may be permanently unavailable, because the basis carryover that defers wash-sale losses in taxable accounts does not apply to IRA cost basis.

In a taxable account, a wash-sale disallowance is added to the replacement shares' cost basis: the loss is deferred, not necessarily destroyed. The investor benefits from that basis adjustment at the eventual sale of the replacement position. When the replacement purchase is in an IRA, the IRA's basis is governed by its own contribution and conversion rules — not by carryovers from disallowed losses in separate accounts. The potential tax benefit from the original harvest may be permanently unavailable rather than merely deferred.

This is the scenario that makes household-level wash-sale awareness most consequential. A spouse who contributes to an IRA or rebalances inside a retirement account in the same week another household account is harvesting a loss may inadvertently destroy that loss — without either broker having visibility into the other side. The substantially-identical analysis still applies: what counts as "substantially identical" covers how practitioners evaluate that question for ETFs, sector funds, and related securities.

Common traps in households that manage accounts at separate brokerages

What are the most common household wash-sale traps when spouses manage accounts at different brokerages without coordinating trades?

The most common household wash-sale traps are automatic dividend reinvestment in one spouse's account while the other harvests the same position, uncoordinated rebalancing where both accounts hold the same broad-market fund, and IRA contributions made in the same period as a taxable-account loss harvest in the same security.

The practical traps, in rough order of frequency:

- DRIP in one account while the other harvests. One spouse sells a stock at a loss; the other has automatic dividend reinvestment enabled on the same stock. A dividend payment inside the 30-day window triggers a wash-sale disallowance on the harvest — silently, with no deliberate trade required.

- Uncoordinated rebalancing in the same index fund. Both spouses hold shares of the same broad-market ETF. One account sells a loss position; the other's automatic rebalancing triggers a purchase of the same ETF inside the window. Each brokerage only sees its own account's activity — neither flags the cross-account conflict.

- IRA contribution in the same period as a loss harvest. An annual IRA contribution that purchases the same mutual fund being harvested in a taxable account can trigger the wash-sale rule, with the permanently-unavailable-loss consequence described in the prior section.

- RSU vesting that overlaps a harvest window. A spouse whose employer grants restricted stock units in a company also held in the other spouse's taxable account may inadvertently create a wash sale when those shares vest inside the harvest window.

How HarvestEngine handles household-pool wash-sale tracking

How does HarvestEngine's household pool feature detect wash-sale risk across accounts at different brokerages?

HarvestEngine lets you group accounts into a shared household pool so its wash-sale impact checking covers exposure across every account in the pool — not just the account where the harvest is occurring — including pending order legs and open proposals in other household accounts.

When the optimizer evaluates a harvest candidate, its wash-sale impact check looks at the tax-lot pool for every account in the same household pool. A same-symbol purchase in a spouse's account — whether from a recent DRIP, a rebalance trade, or a pending order leg — appears in the impact calculation for the harvest candidate in the other account. Pending proposals and open order legs are included in the lookforward window alongside historical lots.

The system applies the same logic to retirement accounts in the pool: IRA purchases inside the 30-day lookback or lookforward window are flagged the same way as taxable-account purchases, consistent with Rev. Rul. 2008-5's reasoning. For the full end-to-end harvest mechanics, TLH 101 covers the workflow from loss identification through proposal execution.

Read this next with the wash-sale rule, demystified, what counts as "substantially identical", the IRS code cheat sheet, and TLH 101.